See exactly what you're buying.

Every worksheet shown here is from the actual file. No mockups.

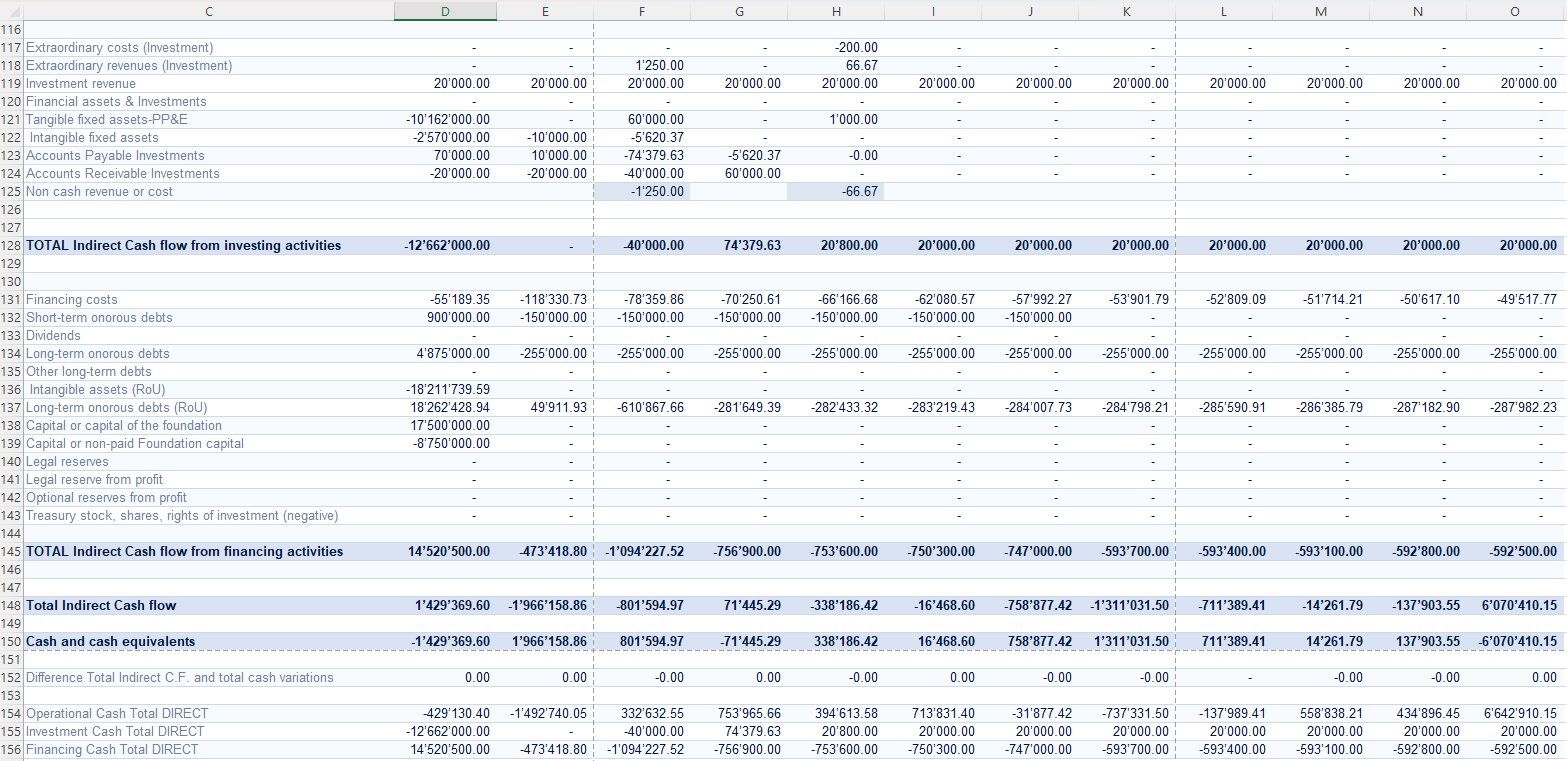

The reconciliation worksheet proves both methods match across all 12 months, broken down by operational, investment, and financing activities. Every check row reads 0.00. This is the single most important worksheet in the model.

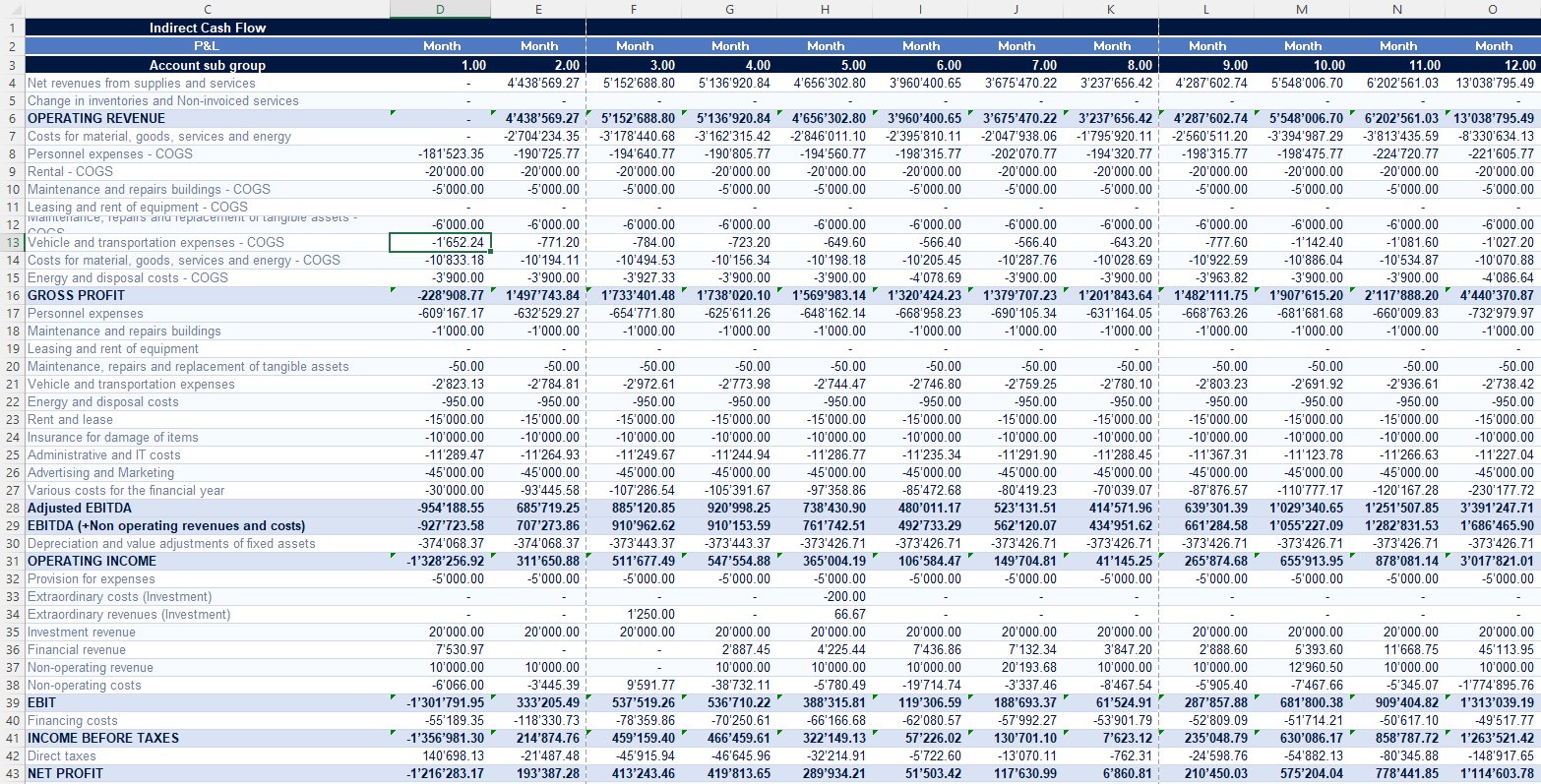

Full P&L with COGS and OPEX separated throughout. Six profitability subtotals: Gross Profit, Adjusted EBITDA, EBITDA, Operating Income, EBIT, and Net Profit. Flows automatically from journal entries, updated every month.

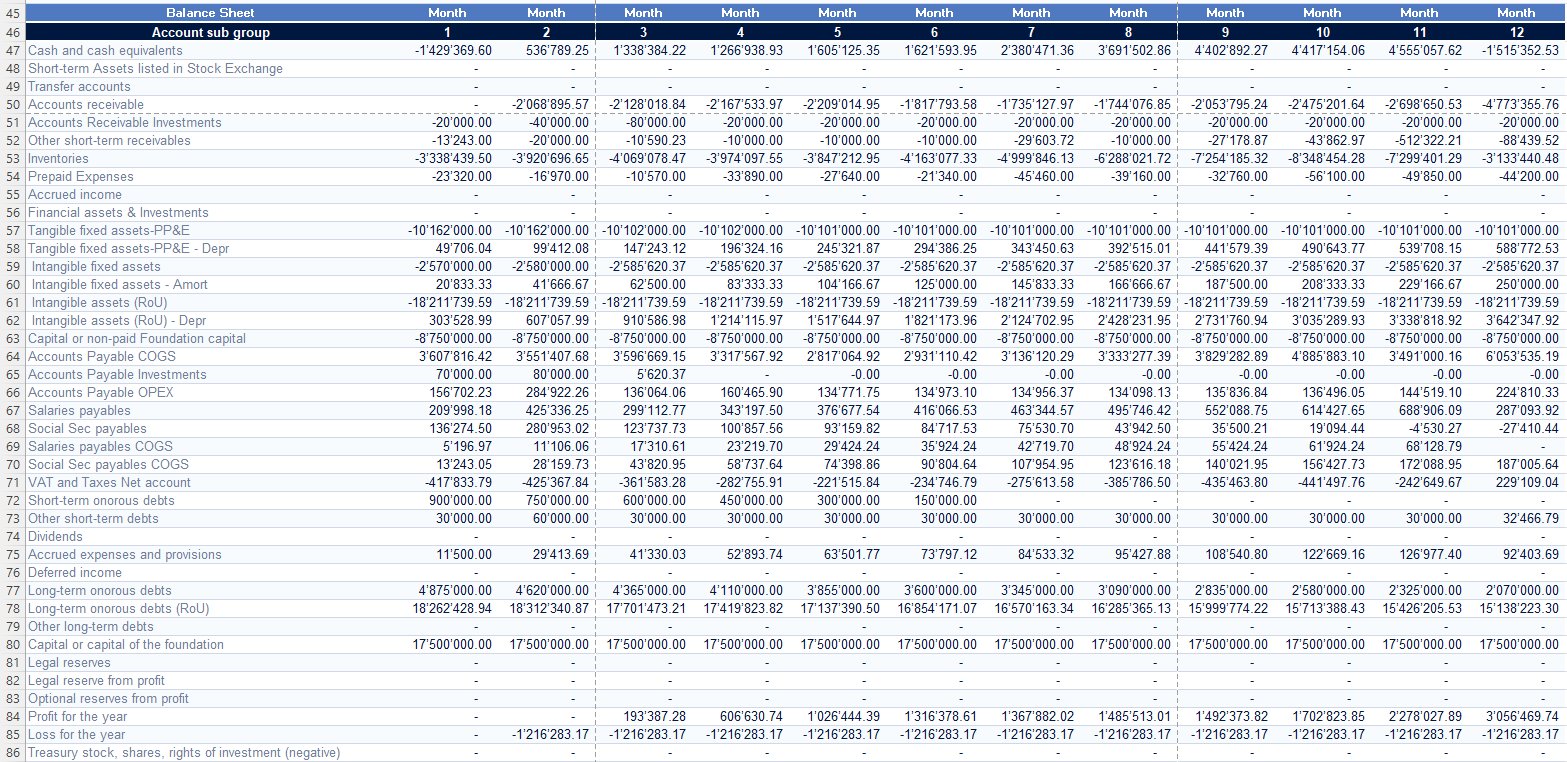

Complete balance sheet updated monthly. Includes right-of-use assets and lease liabilities (IFRS 16), separate payables for COGS, OPEX, and investments, and full equity section with retained earnings tracking.

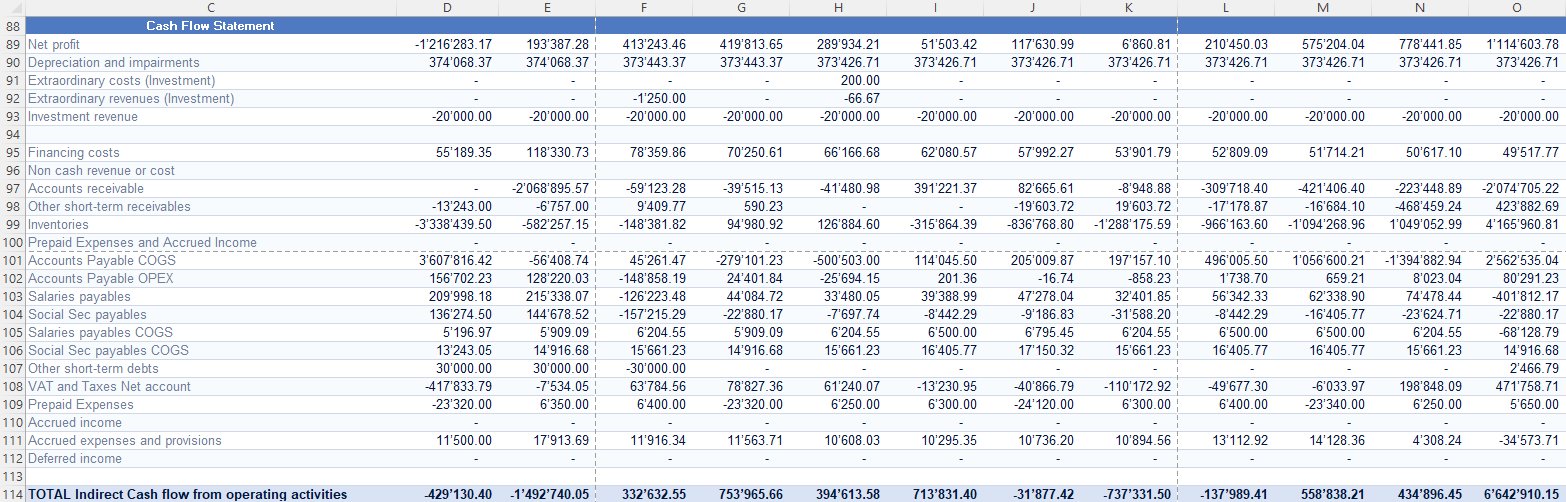

Net profit adjusted for non-cash items: depreciation, working capital movements, inventory changes, payables, receivables, accruals. Every line sourced directly from the balance sheet and P&L. Nothing is manual.

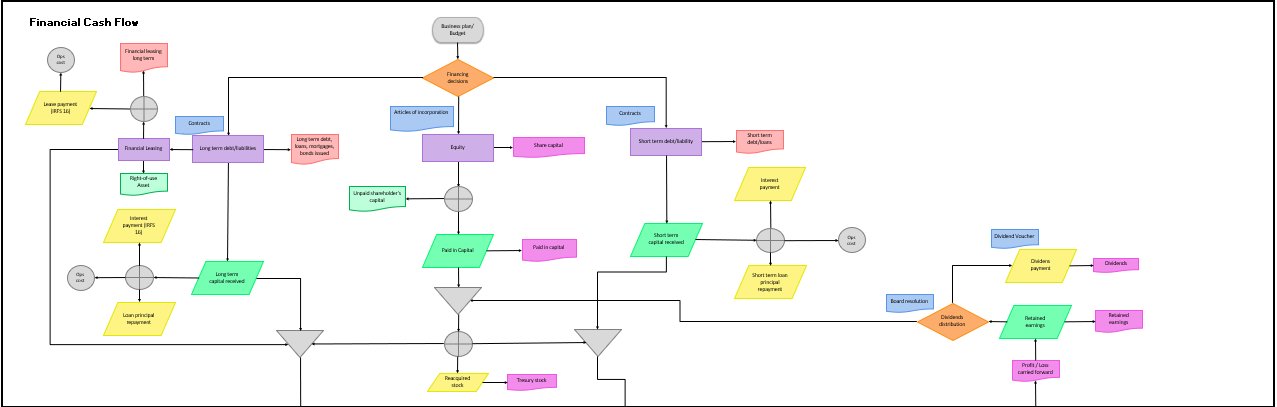

Capital expenditure, intangible assets, long-term debt movements, IFRS 16 lease liabilities, dividends, and equity changes. Fully integrated with the balance sheet so every movement is traceable.

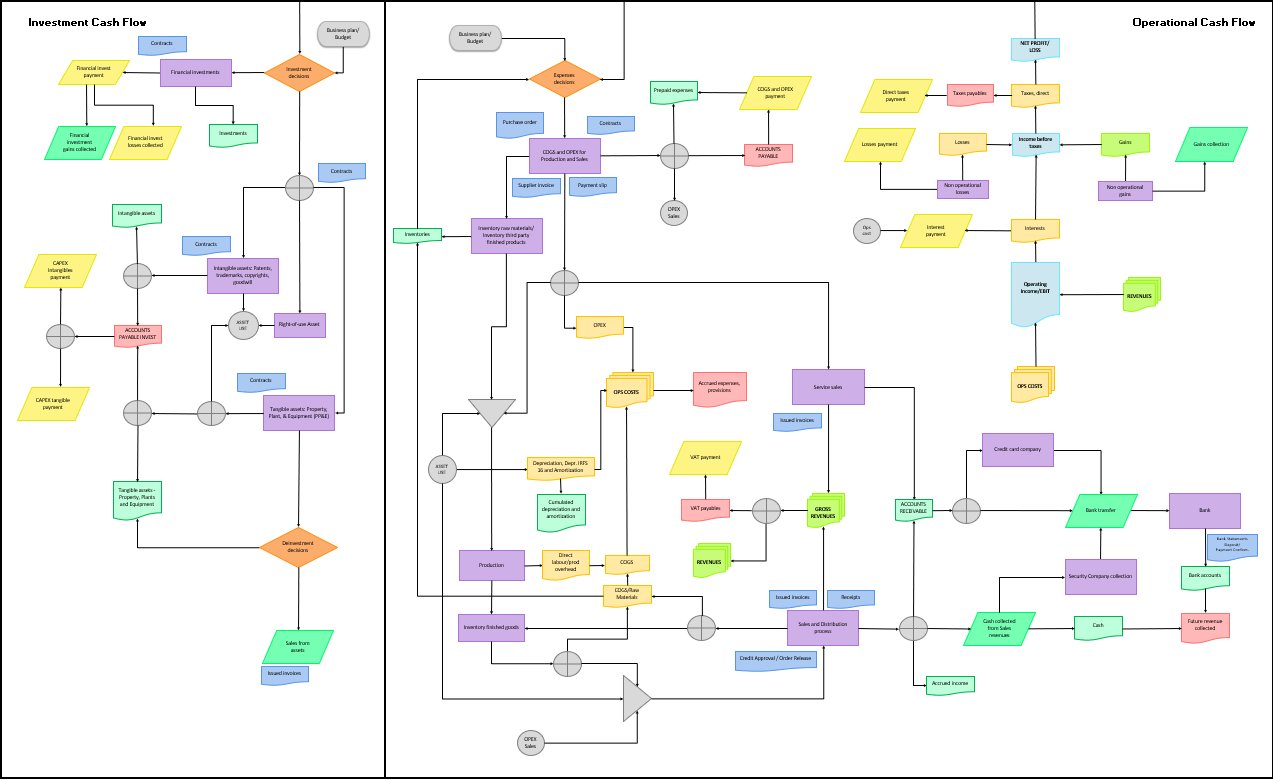

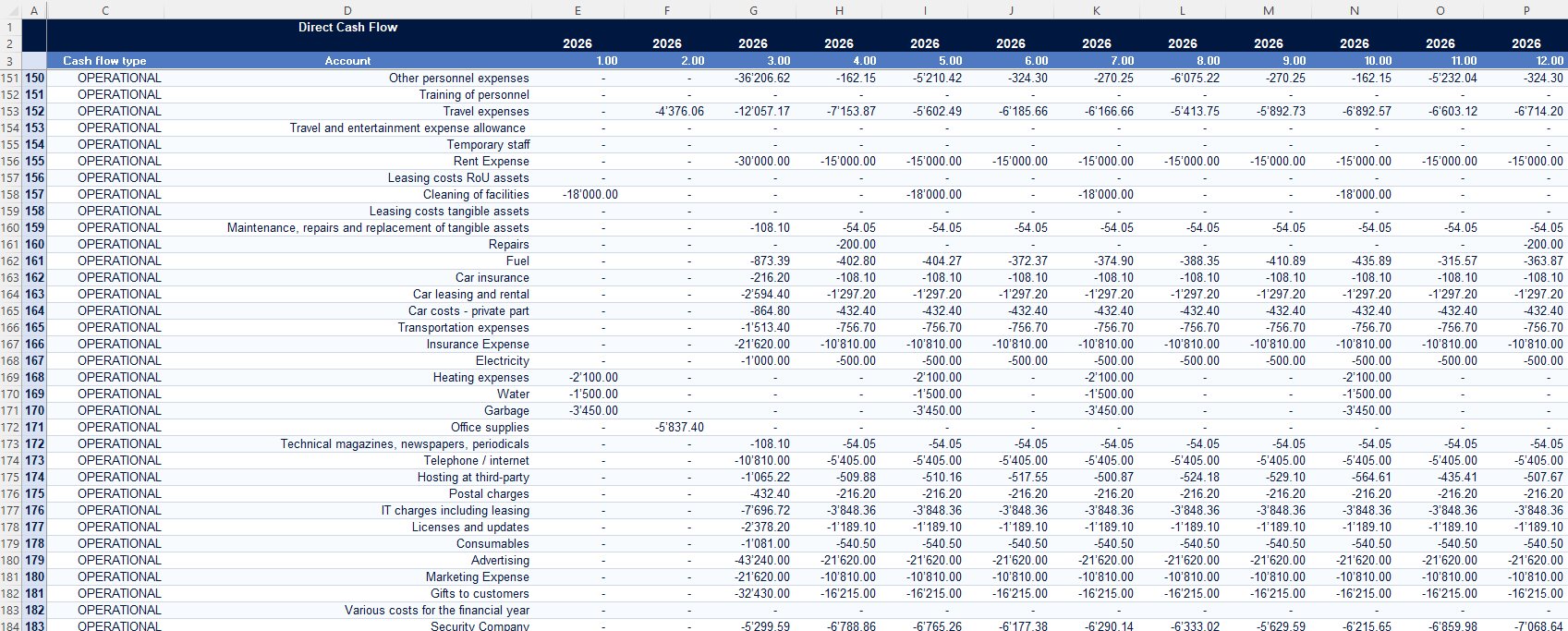

Every actual cash movement classified by type (operational, investment, financing) at individual account level across all 12 months. Built directly from journal entries, not derived from the P&L. Shows exactly which expenses consumed cash and when: the granularity the indirect method abstracts away. Reconciles automatically to the indirect method with zero variance.